How to Transition to a Just Monetary System

Ensuring Socio-economic JusticeKhalil Abdul-Rahman

Muharram 01, 1429 2008-01-10

Occasional Paper

Allah has forbidden you to take usury; therefore all usury obligations shall henceforth be waived. Your capital is yours to keep. You will neither inflict nor suffer any inequity. Allah has judged that there shall be no usury and that all the usury due to Abbas ibn 'Abd al-Muttalib is waived. (Farewell Khutbah)

Let’s reflect on how decisive this guidance is and on how relevant it is in regard to the state of economic and social justice in the world today in the year 1429 A.H. Allah’s Messenger, may peace be with him, calls for the immediate end to all transactions involving usury. (In this document, we make no distinction between usury and interest. Our understanding is that these terms have the same meaning.) Of course this includes all debts, for which now only the initial amount borrowed is due.

Those who had already paid the initial amount and who were paying the usury that was due were immediately relieved of that obligation. And by carrying out all these dramatic changes, we are told that we will not cause others to be treated unfairly and that we will not bring injustice to ourselves.

Unfortunately for all, we have not done our part and we have actually brought injustice to ourselves and to others. The monetary system that dominates the world today is based on usury and on a banking practice called fractional reserve banking that systematically reduces the purchasing power of money. This system is a root cause of widespread debt and unemployment. It manifests itself as one of the most oppressive forces to human society the world has ever known.

We could come to the conclusion that things have gotten so complicated that it would be very difficult to figure out how to fix our situation. Just think, there are just so many transactions involving usury, and many of them are complex. These transactions involve billions of people and affect a wide-range of industries and services. How can we transition to a state where we conduct our financial affairs without usury?

At the top of the list of transitional steps is to

- end all usury obligations immediately, and to

- eliminate the practice of fractional reserve banking.

The first item in the list is shaped by the guidance provided in the Farewell Khutbah referenced above. There is much wisdom in requiring an immediate end to all transactions involving usury. Imagine trying to eliminate usury by allowing Muslim countries to independently determine their timeline for ending transactions involving usury. It would not be possible to fairly and equitably settle debts in this case.

Due to usury, debts would continue to grow over time in those countries that have not yet implemented the change. Muslims in countries that have ended usury will be able to fairly settle debts among themselves, but will not be able to achieve this between themselves and Muslims in the other countries. This highlights the need to not only end usury among Muslims, but also to end it between Muslims and all other people. All debts involving Muslims, whether as the person (or organization) that provided the loan or as the person (or organization) that received the loan, must be made free of usury at the same time.

To explain how this approach to debt settlement brings fairness to people who are not Muslim, it is necessary to discuss briefly the role that money itself plays in the matter. The point to be made is that debts paid with money of intrinsic value provides more value to the payee over a much longer period of time than debts paid with money of no intrinsic value. This is particularly true when realizing that neither the principal part nor the usury part of the original debt was created from money with intrinsic value in the first place.

Money in the role as a medium of exchange makes sense when it has purchasing power that people understand. People today expect money to have a certain purchasing power tomorrow, because of their memory of its purchasing power yesterday. Going back one step, people yesterday anticipated today’s purchasing power, because they remembered that money could be exchanged for other goods and services two days ago.

The purchasing power of money can be traced back through time until we reach the point at which people first emerged from a state of barter. At that point, the purchasing power of the money in use can be explained in just the same way that the exchange value of any commodity is explained. This means that the money itself had value.

Of the various commodities used as money over the span of recorded human history, gold has played the most dominant role by far for more than 2600 years. Because people valued gold for its own sake before it became money, its purchasing power was understood then as it is now. Today, however, the great majority of people do not regard gold as money – a condition brought about by force.

For example, in the United States during the world depression, President Franklin Roosevelt signed Executive Order 6102, which ordered people to turn in their gold to the government at payment of $20.67 per ounce (the value of gold in dollars at that time). Individuals could hold up to $100 in gold coins, but the government through the actions of its central bank known as the Federal Reserve, took the rest with payment in dollars. This order was cancelled approximately 42 years later.

The first impression of this action may suggest that the deal was reasonably fair, given the fact that “equal payment” in dollars was provided. But the dollars themselves were not backed by gold. Monetary inflation, which is the practice of artificially expanding the money supply, produces money in the form of paper that is not backed by anything of intrinsic value. Monetary inflation necessarily leads to a decrease in purchasing power of the basic unit of the currency that is being inflated. Today in 1429 A.H. the dollar buys about one sixteenth as much as it did before the Roosevelt administration.

Consequently, paying debt with money that is not inflated provides much more value over time than paying the same debt with money that is inflated. Note also that no matter how hard someone may try, paying debt effectively means paying only the principal part of the debt. (See the section “Why the Usury Part of a Debt Can Never Be Fully Paid”).

Why the Usury Part of a Debt Can Never Be Fully Paid

When money is borrowed from a bank, the bank actually creates new money or “credit” out of nothing. It credits a loan account it has set up on its books with a deposit that can be used by the borrower. Since banks must pay out deposits on demand, the deposit is a liability for the bank that is entered on the debit side of its ledger. On the credit side of the ledger, because the bank charges usury on this created money, the money borrowed is an asset for the bank earning it income. This is all accomplished by moving some figures from one account to another.

Creating new money out of nothing is, of course, an illusion. As we follow this thread of events we will see that ultimately, the rest of society over an unknown number of generations is held responsible for trying to pay the usury part of a collective debt that is impossible to pay.

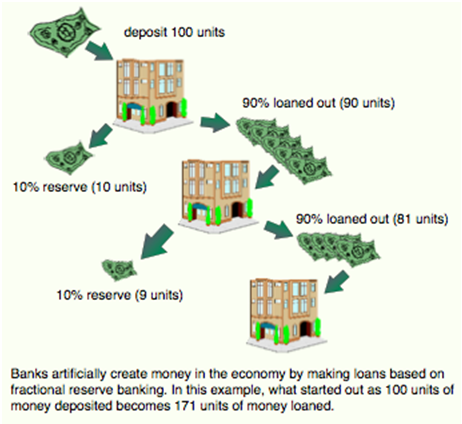

To provide money to the borrower at the time of need, the bank uses money it already has from other depositors. For example, when a bank gets a deposit of 100 money units it could possibly be able to lend out 90 money units. The amount available for lending comes from an agreement between the central bank and the commercial bank providing the loan. In this example, the 10 money units that is not available for lending is called the amount held in reserve and the agreement is called the reserve requirement. Managing reserve requirements in this way is one of the responsibilities of today’s central banks.

The approach to keeping only a fractional part of the original amount deposited in reserve is based on the assumption that all depositors are not likely to want to withdraw at the same time all their deposited money. This practice, called fractional reserve banking, is an essential condition for banks to maximize their potential earnings from usury. It allows banks to take advantage of the time period between the deposit time and the deposit use time of all its depositors.

Exhibit 1. Fractional reserve banking at work.

Using a different example, let’s say that the borrower gets a loan of 1000 money units, spends it while obtaining needed goods and services, then repays an amount of 1100 money units because of the cost of usury. It would appear that the debt has been settled completely. A closer look shows that something differently has happened.

Where did the 100 money units come from that were used to pay the usury part of the loan? If it came from borrowing more money, then the borrower’s total debt just got larger due to additional usury. If it came from providing goods and services to customers, then the prices of those goods and services had to be high enough to provide reasonable earnings to the borrower. This means that the borrower passed on to customers the cost of usury.

But earnings can never increase fast enough to keep pace with usury so long as new loans with new usury components continue to be introduced into the money supply chain. Every such new loan has an inflationary impact on earnings. This puts pressure on organizations to try to find ways to reduce costs in order to make present earnings fulfill their needs. Higher unemployment frequently is one of the outcomes.

Even when money is earned using legitimate means that do not directly involve usury, the indirect consequences of usury have significant impact. Any money that finds it way to a bank will be subjected to a fractional reserve practice of some type. Consequently, this money either will become part of a new loan or will be used in reserve.

Since the amount kept in reserve is so small compared to the amount that becomes part of a new loan, the net effect is to artificially expand the money supply far beyond what physically exists. Today, more than 90 percent of the money in circulation is “credit” or money that originated as part of a debt transaction and exists only as numbers associated with an account.

Returning to the list of transitional steps, it is necessary to

- convert existing currencies in Muslim countries to a common digital gold currency backed entirely by gold,

- convert existing prices of goods and services and amounts of debt to the new currency, and to

- ensure that central banks circulate only money that is 100% backed by gold.

It is important to recognize the significance of what happened in the case of the United States and what happened throughout the world when governments transitioned from a currency that was backed by gold to one that was not. Those governments removed the individual’s legal right to exchange the government’s paper currency for gold or silver coins. What had been a legal obligation of the government to fully convert its currency into either gold or silver coins was removed. Later in this document we call for the central banks of those governments to fulfill this obligation.

How do we get to the condition of being able to pay debts with money that is not inflated? Surprisingly, a lesson can be learned from the world’s central banks and their use of gold. It turns out that though the public does not regard gold as money, central banks do.

The practice of monetary inflation is a fundamental part of the operation of governments throughout the world today. Through the function of central banks, governments expand their money supply by printing paper money in the form of the currency that represents their country. When central banks artificially expand (and contract) the money supply, they are attempting to manage their countries’ monetary system in ways that make sense to them.

Since economic forces are so very complex and since no country can conduct its affairs entirely independently of all other countries, the interplay of world economic forces presents a management challenge that no combination of central banks is able to meet. Among the consequences of poor monetary system management is high government and society debt, devaluation of currency over time, and widely fluctuating exchange rates among world currencies.

But while central banks and their governments impose an inflated paper currency on their citizens, these banks conduct business among themselves in a fundamentally different manner. Take for example one of the functions of the Federal Reserve Bank of New York, the largest of the 12 banks that make up the Federal Reserve System in the United States. This bank serves as one of the largest gold repositories in the world, acting as a guardian of the gold owned by many foreign nations, central banks, and international organizations.

The bars of gold are tagged according to the owner and stored in a secured vault that lies 26 meters (85 feet) below sea level. Employees in the vault move these bars back and forth into appropriate piles. In essence, this is how central banks clear their accounts with each other. Some central bankers still believe that gold is money, but only for central bankers.

Now let’s work from the point of view that Muslims regard gold as money. All the Muslim countries would introduce a new common currency that would be backed by 100% gold reserves. Let’s call it the Islamic State Dinar for this discussion. This new currency would represent a fixed weight of 22K gold. It would be a digital gold currency that would be divided in parts as needed to accommodate the currency conversion requirements and the pricing requirements of goods and services. This type of currency is an electronic form of money that represents a specified weight of gold.

At the same point in time that all transactions involving usury are ended, the central banks of all Muslim countries would stop printing paper money that has no intrinsic value and would be reformed to put into circulation only the new Islamic State Dinar. Preparing for the eventual conversion of an existing currency to the new currency, use the then existing world price of gold to establish a gold value relationship between gold and the existing currency of a country.

For example, today in 1429 A.H. one gram of gold is equivalent to 103 Malaysian Ringgit or 1,877 Pakistan Rupee or 282,036 Iranian Rial. If one Islamic State Dinar equals 0.05 gram of 22K gold, then the following would be approximately true:

5 Malaysian Ringgit= one Islamic State Dinar

94 Pakistan Rupee = one Islamic State Dinar

14,102 Iranian Rial = one Islamic State Dinar

Using the relevant conversion factor, people and organizations possessing an existing currency would purchase the new currency from a reformed central bank. Central banks, commercial banks, and other financial institutions would fulfill the responsibility of converting existing accounts to the new currency. All the money in circulation in Muslim countries would be converted to the new currency, therefore preventing any loss of money (monetary deflation).

The ease of this transition largely depends on the willingness of the financial institutions to reform and their commitment to function cooperatively with each other. Central banks, for their part, play a key role because they manage the gold holdings of their countries. Exhibit 2 shows the amount of gold held in reserve in the year 1428 A.H. by central banks of some Muslim countries.

Exhibit 2. Gold reserves in selected Muslim countries (Source World Gold Council)

| Algeria | 173.6 |

| Libya | 143.8 |

| Arabia | 143 |

| Turkey | 116.1 |

| Kuwait | 79 |

| Egypt | 75.6 |

| Indonesia | 73.1 |

| Pakistan | 65.3 |

| Kazakhstan | 62.7 |

What needs to be emphasized here is that any amount of gold collectively held in all the central banks of Muslim countries would work. And it could work regardless of the number of people involved, and regardless of the number and complexity of commercial transactions that could take place over time.

This is true because in the absence of usury, hoarding of money, and artificial monetary expansion and contraction, the amount of the existing money supply would adjust due to free market forces so that all of society’s needs would be met. In this context, gold would be actively bought, sold, traded, imported, and exported. Additionally, prices would be free to move in the direction determined by market forces. It is the purchasing power of money that is important, not the amount.

To avoid any immediate change in the purchasing power of the new currency as compared to the purchasing power of the currency it replaces, the existing prices of goods and services and debts without usury would also be converted to the new currency. As emphasized earlier, all these events would need to occur at the same point in time.

A monitoring/auditing system would need to be established to ensure that all the central banks stay true to only putting the new currency in circulation that is 100% backed by gold. This system would also be used to confirm that all banks and financial institutions no longer loan money involving usury. Under the new monetary system, computerized record-keeping, electronic money transfers, ATM machine transactions, and other emerging technology developments could continue to take place rapidly and smoothly as they do now.

Related Articles